The Ukrainian Council of Defence Industry, together with CORE Team, has presented new research into the labor market and salary landscape within Ukraine’s defense sector. A survey of 27 defense manufacturers found that the industry is scaling rapidly: 100% of surveyed companies plan to hire new staff over the next 6–12 months. However, the biggest constraint on further growth remains the shortage of qualified engineering and technical specialists.

The sample included Ukrainian manufacturers operating in ground robotic systems, UAVs, dual-use technologies, electronics, components manufacturing, miltech software, electronic warfare (EW), and related sectors.

According to the survey, 74% of companies expanded their teams by at least 25% over the past year, while nearly half reported growth by more than 50%. None of the companies surveyed plan to freeze recruitment: 48% expect significant expansion, while a further 52% anticipate moderate growth.

“The Ukrainian defense industry is no longer a narrow niche. It is now a distinct labor market requiring engineers, manufacturing specialists, procurement professionals, project managers, quality assurance experts, export specialists, and partnership managers simultaneously. The sector is growing rapidly, but its ability to scale further will depend on whether we can systematically train people for the real needs of production,” said Ihor Fedirko, CEO of the Ukrainian Council of Defence Industry.

The strongest demand is for design engineers, with 67% of respondents actively recruiting for these roles. Manufacturing personnel and assembly specialists rank second, with 56% of companies searching for these candidates. There is also strong demand for electronics engineers, embedded systems engineers, software developers, and project and product managers.

Engineering positions remain the most difficult to fill. Some 48% of respondents identified both design engineers and electronics engineers as particularly scarce. Other hard-to-fill roles include software developers, embedded systems engineers, CNC machine operators, technical specialists, procurement and supply chain professionals, and quality control specialists.

The key challenge to hire qualified professionals is not limited to salaries alone. Forty-four per cent of companies cited the lack of candidates with the required qualifications as the primary barrier. 33% of Defense Tech market players pointed to intense competition between companies for the same limited pool of specialists. The median time required to fill a technical vacancy is between one and two months, while nearly 30% of such vacancies remain open for more than two months.

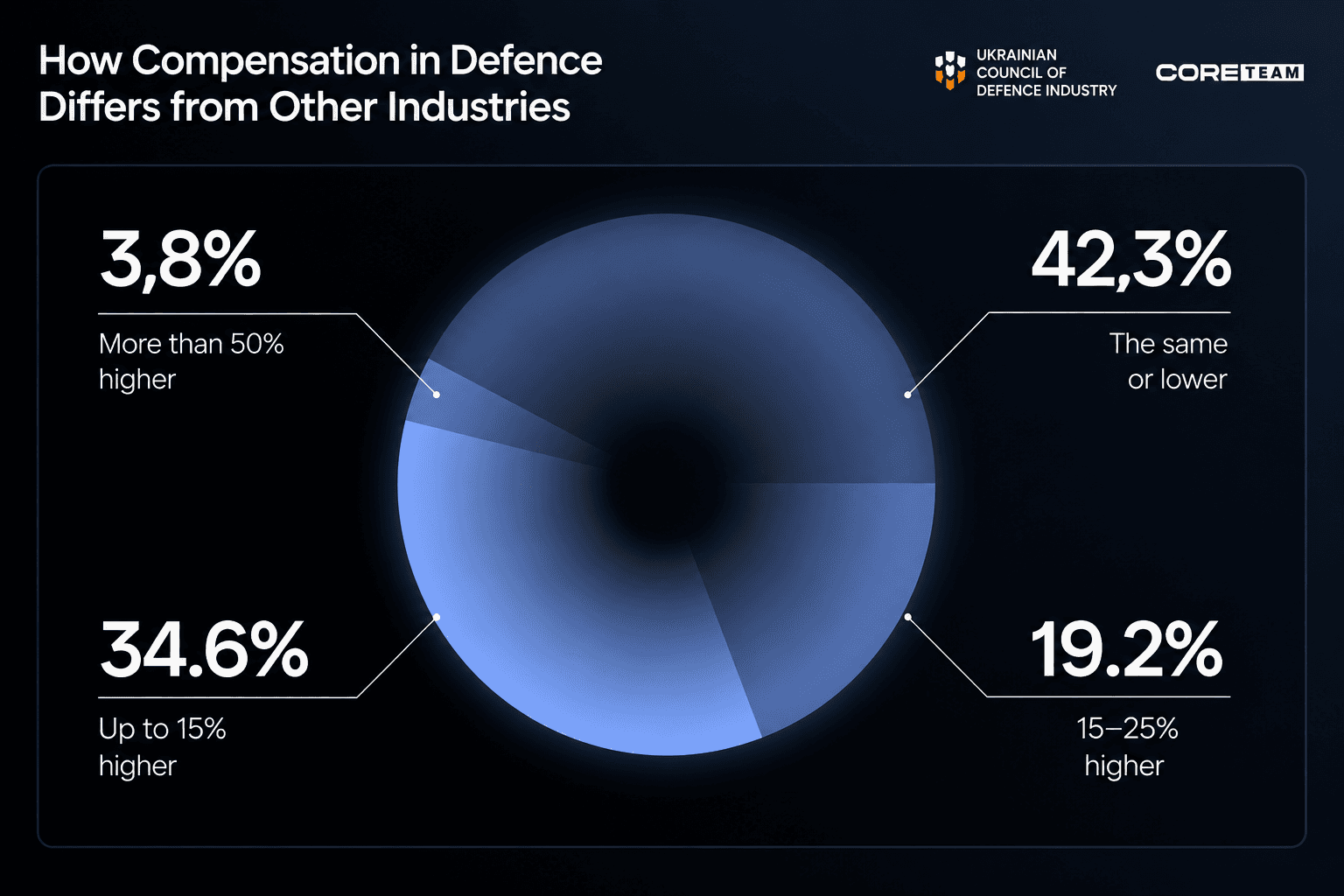

The research also highlights important salary trends. Eighty-nine per cent of companies reviewed salaries over the past year, either across the board or for selected roles. The most common increase was between 10% and 20%. However, salary increases alone did not resolve recruitment challenges: not a single company reported that hiring became significantly easier following pay reviews.

The findings also challenge the simplified assumption that the defence industry always pays above market rates. Forty-two per cent of companies stated that their salaries are at or below levels seen in other sectors. While salary premiums do exist, they are highly selective and concentrated in shortage areas such as embedded systems engineering, electronics, radio frequency technologies, electronic warfare, avionics, hardware engineering, and selected procurement and supply chain roles.

Another major factor in competition for talent is an exemption status. Some 74% of companies offer exemption as an employment benefit, and for many candidates this is no less important than salary levels.

“The market has already moved beyond the phase of emergency hypergrowth towards more structured scaling. Companies no longer need only a handful of strong engineers — they require entire teams covering R&D, manufacturing, testing, quality assurance, procurement, exports, legal support, and regulatory compliance. This means that workforce policy for the defense industry must become just as systematic as industrial policy itself,” the report concludes.

When asked about the sector’s key needs over the next one to two years, companies most frequently cited a larger engineering workforce and greater predictability of orders, both mentioned by 56% of respondents. This suggests that the staffing challenge is directly linked to contract stability: without predictable demand, companies struggle to plan recruitment, retain talent, and invest in training.

In addition, 48% of companies called for stronger cooperation with universities, while 41% highlighted the need for more retraining programs. Increasingly, the sector is forced not only to compete for ready-made specialists, but also to develop talent internally or recruit professionals from adjacent industries. The largest sources of talent for the defense industry are mechanical engineering and industrial manufacturing sectors, cited by 59% of companies, followed by IT, mentioned by 44% of respondents.

"What we see in Ukraine today, Western defence industries are likely to face within the next three to five years. Every company we surveyed plans to expand, yet the market simply does not have enough engineers to support these growth plans. Traditional recruitment has reached its limits. The companies that will have a competitive advantage are those already building their own talent pipelines through partnerships with universities, reskilling professionals from adjacent industries, and investing in internal academies. This is no longer just an HR challenge — it is a critical component of industrial and defence capability," said Anna Korol, CORE Team Founder.

KEY RESEARCH FIGURES

The research primarily reflects the fast-growing manufacturing and technology segment of Ukraine’s defense industry. While it does not represent the entire defense-industrial complex, it offers an important snapshot of how a new labor market is emerging within Ukraine’s defense technology sector — one where demand for talent is growing alongside production capacity, technological complexity, international cooperation, and the need for sustainable scaling.

Anna Korol

CORE Team CEO